Buck Whizz: The rise and fall of global currencies is a process which reflects new realities

The advantages accrued to the United States by its dollar being the world’s leading safe-haven asset are legion and ultimately help succour American power. Indeed, the US dollar’s status as the predominant reserve currency is known as the ‘exorbitant privilege’, enabling the country to borrow a lot of money relatively cheaply.

Though economists and historians may argue about how long this privileged position may last in a rapidly changing world, there is less dispute over the numerous benefits it brings to the US economy, businessaes and consumers. Enzio von Pfeil, a prominent financial commentor in Hong Kong, cites the US Treasury’s ability to issue as much debt as it wants as a key bonus, as well as the elimination of transaction costs. “All of America’s international transactions are done via her own US dollar, thus obviating any foreign exchange risk as well as foreign exchange conversion costs,” he says.

US government debt is also cheaper than that issued by non-reserve currencies. “Most reserves are held in US Treasury bills and bonds. Thus, strong global demand for USD Treasuries means that their yields are low,” explains von Pfeil, highlighting how the government can infinitely fund its federal debt at very low rates.

Financial gains

Other financial advantages derive from the depth of the dollar-dominated global payments system – all global US dollar transactions are easily processed via Swift (the interbank financial telecommunications network) – and the US dollar’s broad acceptance. American consumers also benefit from the willingness of countries to hold the US dollar as part of their reserves portfolio since this cushions their exchange rate.

As Professor Kent Matthews of Cardiff Business School in the United Kingdom outlines, short-term inflows and outflows are absorbed by the global currency markets without much change in the price of the dollar. “This means that the dollar exchange rate has a marginally higher value relative to other currencies. This is the dollar premium,” he says.

There are political advantages, too. “Owning the world’s predominant currency, the Americans can weaponise it by freezing another nation’s dollar assets, denying other nations any access to the dollar, or blocking their access to Swift,” notes von Pfeil.

Historical fluctuations

However, having a powerful global currency can also be a curse. “The yen and the pre-euro Deutschmark resisted attempts by the global market to make them larger internationalised currencies because upward pressure on their respective exchange rates would hurt their exporters,” explains Matthews of Japan and Germany’s export-led economies.

While any credible challenge to US dollar supremacy remains a subject of speculation, the same was once said of the British pound, which had prevailed for a century in the Pax Britannica period prior to the First World War (1914-1918). “Sterling lost its dominance because the immutability of its value was lost as it was weakened after the First World War. Its net foreign asset position declined dramatically after this war, and fell to zero after the Second World War,” says Matthews.

“It was losing in terms of trade dominance and capital dominance. At the same time there was a credible alternative,” he adds, referring to the eventual succession of the US dollar.

Dollar supremacy

Jean-Marie Mercadal, CEO of Hong Kong-headquartered Syncicap Asset Management, points out that the supreme strength of the dollar as the international currency of reference is justified in several respects – including that the US is the world’s largest economy with more than 25% of global GDP; US equities account for nearly 65% of international equity indices; it is the greatest military power; US soft power is strong, culturally and technologically; and the dollar is accepted everywhere.

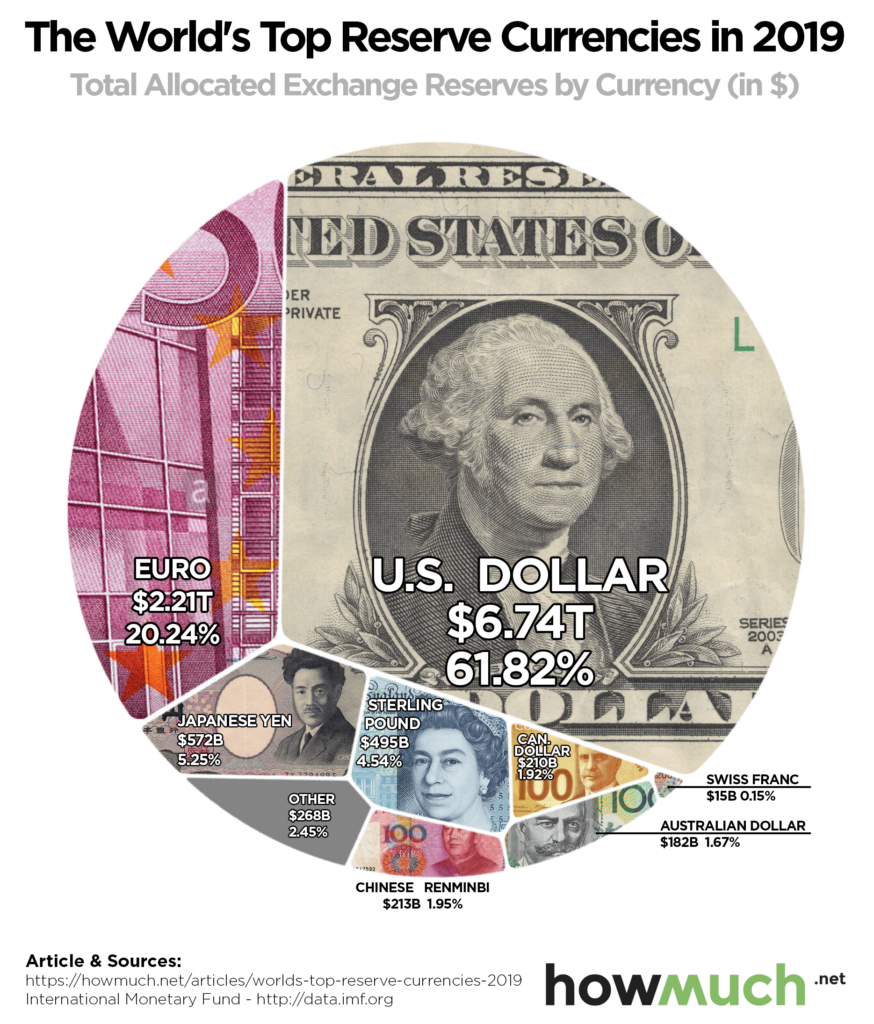

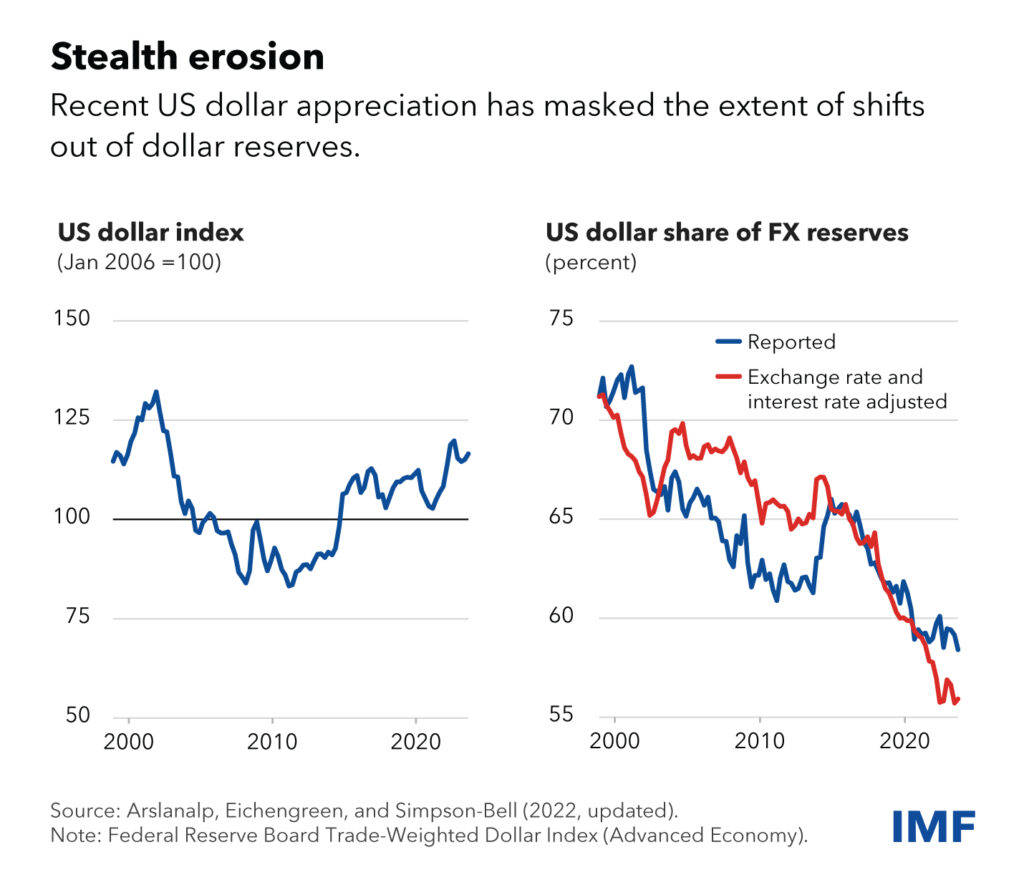

This all-powerful position of American economic and political dominance is echoed in financial statistics cited by von Pfeil: “88% of foreign exchange trades involve US dollars; 80% of all foreign trade is conducted in US dollars, and about 60% of all foreign currency reserves consist of US dollars.”

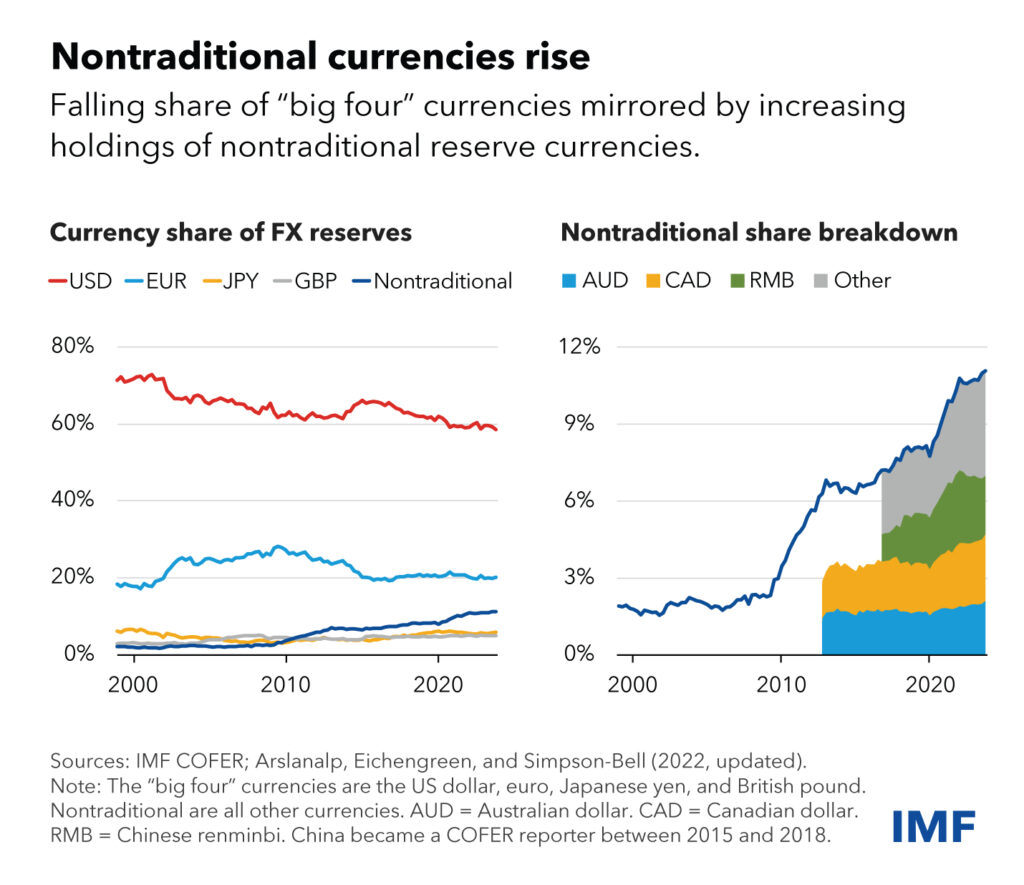

At this stage, von Pfeil sees no real prospect of the dollar being usurped; the euro, the world’s second most important currency, commands just 20% of global total reserves. He also notes that any moves to create a Brics – the Brazil, Russia, India and China-founded international organisation – digital currency or gold-backed stablecoin are still in their embryonic stages, plus such initiatives could be derailed by internal competition between its member states.

Rise of the renminbi?

The renminbi, von Pfeil believes, is not ready to be a contender. “The yuan is a controlled currency, meaning that the RMB is neither freely convertible nor tradeable,” he says, also pointing to a dwindling share of renminbi global forex reserves since 2022. Furthermore, there is no legal framework for global renminbi transactions on the scale, or with the depth, of Swift.

According to Matthews, Beijing’s tight control of fund flows under its capital account is the standout hurdling block to the yuan becoming the dominant currency. He acknowledges that “the renminbi is a threat to the dominance of the dollar” but only in the long term in the event of further relaxation of flow restrictions.

Other financial experts are more bullish about the currency of the world’s second-largest economy, and highlight that the US dollar is beginning to face competition from the renminbi. In March last year, the latter overtook the dollar to become the ascendant currency in China’s own cross-border payments, according to China’s State Administration of Foreign Exchange. “China now exports more than 50% to other emerging countries that can be paid in renminbi that they get in return for their sales of raw materials,” says Mercadal. “Saudi Arabia, for example, sells oil to China and buys high value-added manufacturing goods in return, such as solar panels.”

He sees great significance in such transactions, noting that compared to 20 years ago China now has a wealth of high-quality manufactured products to trade, attracting countries that can pay with commodities or agricultural goods.

Risks and rewards

Despite this, the ability to settle trades in renminbi alone is unlikely to boost its use, according to Sam Kima, Senior Vice-President of bullion services provider First Gold. He points out that the volume of such trades depends on exporters’ willingness to accept the currency for payment, which in turn depends on their ability to use the yuan accrued.

“As the renminbi is not broadly used in international trade and finance, there are relatively few outlets to spend these proceeds. Cumulating the inflow would therefore incur substantial costs and raise currency risks,” he says. “The yuan may gain ground through bilateral agreements and economic growth, but the dollar’s established trust, transparency and stability give it a significant advantage.

“Furthermore, the US political system, despite its complexities, provides a stable and predictable environment for investors. The rule of law, property rights and institutional stability in the US create a favourable climate for the dollar to remain the preferred reserve currency.”

Money as a weapon

Perversely, any real threat to the US dollar could be as a result of its strength. Von Pfeil explains: “Weaponisation is the key threat to the popularity of the US dollar. If a country knows that its US dollar assets will be frozen (step in Russia), or that it will be denied access to US dollars, not to mention denied access to Swift, then why trade in US dollars?”

Escalating geopolitical events, shifting national interests and growing non-US trade, particularly with Asia, have spurred some emerging economies to consider diversifying their external relations. “Countries in the Middle East and North Africa are becoming acutely aware of the risks emanating from their dependence on the US dollar. Dollar dependence also limits their economic sovereignty by increasing their vulnerability to fluctuations in the US economy,” says Kima, who notes that higher international borrowing costs from hikes in US interest rates are another concern.

As many commentators indicate, any shift from one currency dominance to another can take several decades. “For now, there are no real competitors to the dollar,” affirms Mercadal. “The renminbi is not yet freely convertible, and the euro is a political construct that can be fragile.”